The U.S. lumber market moved through 2025 under pressure from weakening residential construction demand, falling employment and a sharp reduction in softwood lumber imports. While sawmill production held steady in the third quarter, the broader picture pointed to a sector facing tighter conditions, particularly as higher import duties began to weigh more heavily on trade flows.

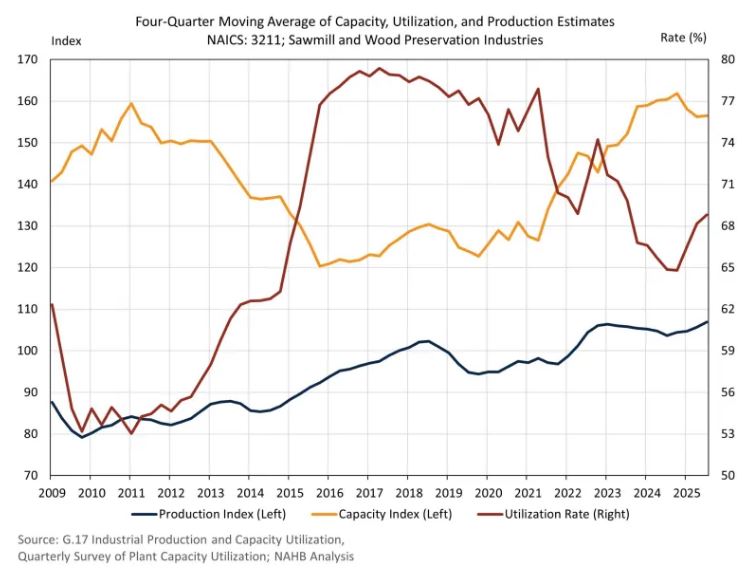

According to the Federal Reserve’s G.17 Industrial Production report, U.S. sawmill production was unchanged in the third quarter. At the same time, utilization rates in sawmills and wood preservation industries remained near 70%, despite softer demand linked to lower residential construction activity during the same period.

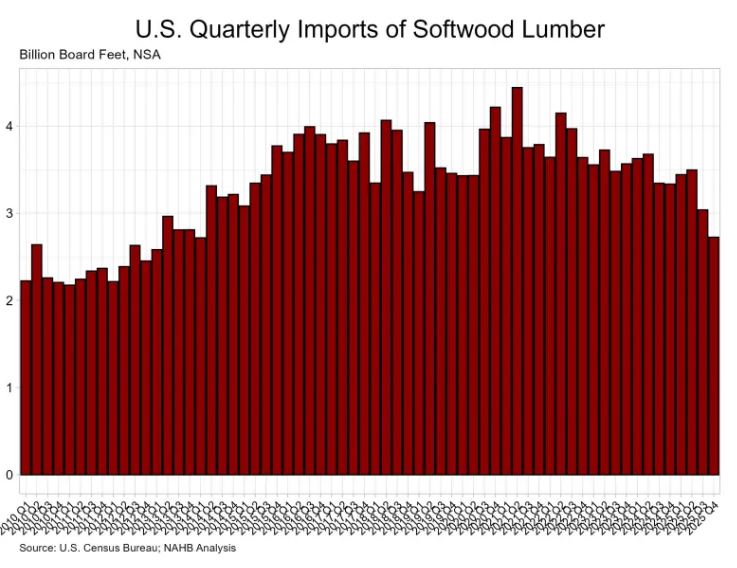

One of the most notable developments of the third quarter was the steep decline in U.S. softwood lumber imports, as higher duties came into force. Over the full year of 2025, the United States imported an estimated 12.7 billion board feet of softwood lumber, the lowest annual level recorded since 2014.

The sawmill utilization rate, which is published quarterly by the Census Bureau and measures actual output relative to full production capacity, has generally trended downward since 2017 due to capacity additions and stagnant production. However, on a four-quarter moving average basis, the utilization rate improved in the third quarter of 2025, rising from 68.2% to 68.8%. Sawmill production also edged higher on the same basis, standing 1.2% above the second quarter and 3.1% higher than the same period a year earlier.

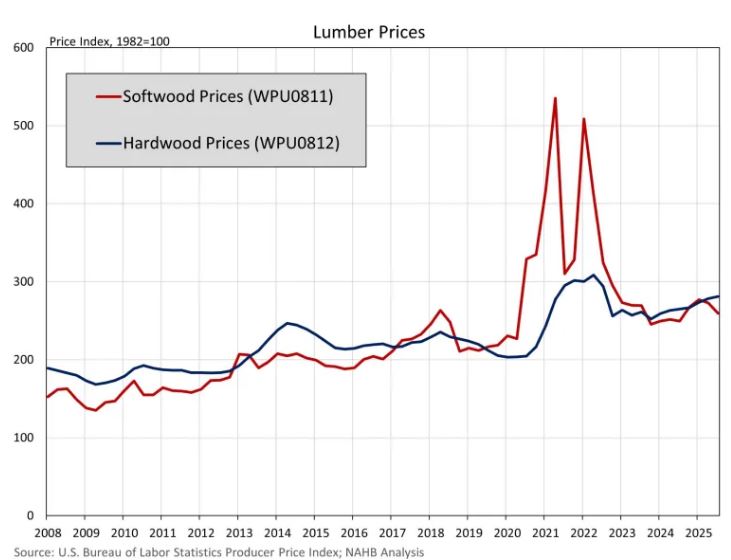

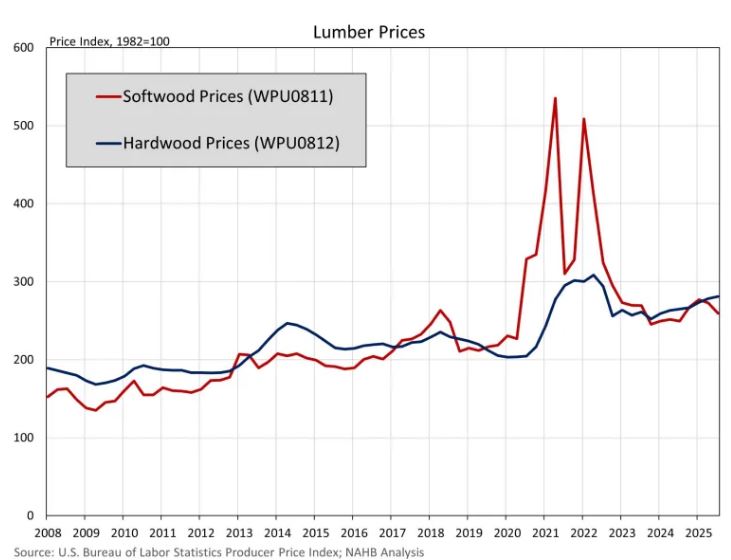

Price movements remained mixed across lumber categories. Softwood lumber prices fell by 4.9% during the third quarter, although they were still 3.9% above year-ago levels. Hardwood lumber, by contrast, continued its upward trend, rising 1.0% in the third quarter. That marked the seventh consecutive quarter of hardwood price increases.

Employment conditions in the sector weakened further. Jobs in sawmill and wood preservation industries declined to around 85,400 workers in the third quarter, marking the tenth consecutive quarterly drop. This pushed employment below the levels seen at the beginning of the pandemic and brought it to the lowest point since the first quarter of 2013.

Import conditions became more difficult throughout the year as duty rates on U.S. softwood lumber imports increased. Canadian shipments were hit hardest, with combined antidumping and countervailing duties doubling to 35%. In addition, all softwood lumber imports became subject to a new 10% Section 232 duty starting in October. As a result, Canadian softwood lumber, which accounts for roughly 80% of all U.S. imports, now faces a total duty burden of 45%.

These higher duties contributed to weaker import volumes in both the third and fourth quarters. Import levels in the fourth quarter fell to their lowest point since the first quarter of 2014. At the same time, duties were not the only pressure on the market, as demand from residential construction continued to soften over the course of 2025.

Source: eyeonhousing.org