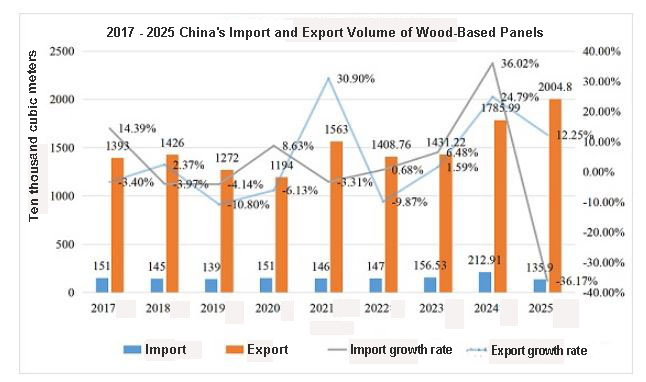

China’s wood-based panel trade expanded in volume during 2025, with total imports and exports reaching 21.407 million cubic meters equivalent, up 6.62% from the previous year. In value terms, however, the combined total fell to US$7.638 billion, representing a year-on-year decline of 2.84%.

The stronger overall volume performance was driven primarily by exports. China exported 20.048 million cubic meters equivalent of engineered wood products in 2025, marking a 12.25% increase compared with the previous year. Export value rose more moderately, reaching US$7.104 billion, up 2.53%. Imports, by contrast, fell sharply. Total imports dropped to 1.359 million cubic meters equivalent, down 36.17% year on year and marking the first decline in six years. Import value stood at US$534 million, down 3.92%.

Plywood exports remained firm while imports fell sharply

In the plywood segment, China’s exports reached 13.573 million cubic meters in 2025, increasing 2.9% from the previous year. Export value totaled US$5.169 billion, although this was 1.9% lower year on year. Imports of plywood dropped much more steeply, falling 58.08% to 331,200 cubic meters, while import value declined 31.98% to US$293 million.

Russia remained the dominant origin for plywood imports, accounting for more than 80% of the total. On the export side, China’s main plywood destinations were largely unchanged. The top five markets were the Philippines, the United Arab Emirates, the United Kingdom, Saudi Arabia and Nigeria. One notable shift was that Taiwan, China, which had ranked fifth in 2024, dropped to 14th place, while Nigeria entered the top five.

Fiberboard posted strong export growth

China’s fiberboard exports recorded a significant increase in 2025. Total exports reached about 4.975 million cubic meters equivalent, up 29.89% year on year. Export value rose to US$1.557 billion, a gain of 14.49%.

Imports of fiberboard products were far smaller in scale, totaling approximately 83,000 cubic meters equivalent, which was still 12.16% higher than the year before. However, import value fell 6.11% to US$43.82 million. The main export destinations for fiberboard remained broadly stable, with Vietnam, Saudi Arabia, Mexico, Nigeria and the United Arab Emirates occupying the top five positions.

Particleboard exports overtook imports for the first time

A major shift in 2025 came in the particleboard segment, where exports exceeded imports for the first time. China imported 944,400 cubic meters equivalent of particleboard during the year, down 25.16% from 2024. Import value fell even more sharply, dropping 55.4% to US$293 million.

The leading sources of particleboard imports remained broadly the same, with Thailand, Brazil, Poland, Romania and Germany ranking as the top five suppliers.

At the same time, China’s particleboard exports rose sharply to 1.50 million cubic meters equivalent, up 78.64% year on year. Export value increased 26.0% to US$378 million. The top export destinations were South Korea, Taiwan, Vietnam, Mongolia and Chile.

Compared with 2024, the rise of South Korea was particularly notable. The country moved from tenth place to become the largest export destination. This change is believed to reflect several factors, including tariff reductions under RCEP, closer China-South Korea cooperation in building materials, a recovery in South Korea’s real estate market and renewed activity in its furniture manufacturing sector.

2026 seen as a transition year for trade quality and structure

Looking ahead, 2026 is expected to be an important transition point for China’s engineered wood panel trade, shifting from a phase of scale expansion toward one focused more heavily on quality and efficiency. Key trends are expected to include larger export volumes, firmer average prices and a more optimized trade structure.

Against this backdrop, companies are expected to place greater emphasis on green standards, product upgrading and market diversification, while working to avoid destructive price competition and rising trade-related risks.